Contents:Exquisite Indian Wedding Invitation Designs to Set the Perfect Tone for Your Big Day!Winning At…

Unearned Revenue Enables Matching When Buyers Pay in Advance

Content

While you have the money in hand, you still need to provide the services. This requires special bookkeeping measures to make sure you don’t forget about your customer and to keep the tax authorities happy. Baremetrics provides an easy-to-read dashboard that gives you all the key metrics for your business, including MRR, ARR, LTV, total customers, and more.

Is all unearned income taxable?

For the most part, unearned income is taxed the same as earned income. However, there are some key differences worth noting. To start with, unearned income is not subject to Social Security or Medicare payroll taxes as earned income is.

Unearned revenue is not an uncommon liability; it can be seen on the balance sheet of many companies. In automated systems, you can define rules that can determine the event which triggers the revenue recognition. Till the time that recognition event is triggered, the amount remains parked in an unearned revenue account unearned revenue as a liability. If you enter an invoice with a Bill in Advance invoicing rule, Receivables creates the following journal entries. Unearned revenue can be applied in almost all industries however it becomes very important in the case of some industries where advance payments are the norm like subscriptions for magazines.

Unearned Revenue in Accrual Accounting

At the end of each month for the next 12 months, the company can recognize a revenue of $125 monthly. Suppose a design software costs $1,500 annually and is required to be paid upfront so that customers can begin using the product. Most large corporations use the accrual accounting method and are required to follow GAAP . Allocate that amount on your books to recognize the revenue once the business obligation has been satisfied.

We Stand by our Reviews and when you Purchase something we’ve Recommended, the commissions we receive help support our Staff and our Research Process. In our previous example, this would be whenever the magazine company actually sends out the next issue of its magazine. Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts. By subscribing, you agree to ProfitWell’s terms of service and privacy policy.

Join over 140,000 fellow entrepreneurs who receive expert advice for their small business finances

Suppose a customer pays $1,800 for an insurance policy to protect her delivery vehicles for six months. Initially, the insurance company records this transaction by increasing an asset account with a debit and by increasing a liability account with a credit. After one month, the insurance company makes an adjusting entry to decrease unearned revenue and to increase revenue by an amount equal to one sixth of the initial payment. Other https://www.bookstime.com/ names used for this liability include unearned income, prepaid revenue, deferred revenue and customers’ deposits. Once goods or services have been rendered and a customer has received what they paid for, the business will need to revise the previous journal entry with another double-entry. This time, the company will debit its unearned revenue account while crediting its service revenues account for the appropriate amount.

- Once the $1200 has been received, the company enters this amount as a credit to unearned revenue.

- Unearned revenue is the money paid by a customer for goods or services that a company has yet to deliver.

- In order to get this deal, the customer is required to pay the company in full on the spot.

- A wide range of different industries make use of deferred or unearned revenue.

- After one month, the insurance company makes an adjusting entry to decrease unearned revenue and to increase revenue by an amount equal to one sixth of the initial payment.

Your business receives the money upfront, and then does the work to earn it at a later date. Unearned revenue is recorded on the liabilities side of the balance sheet since the company collected cash payments upfront and thus has unfulfilled obligations to their customers as a result.

How to Record Unearned Revenue

Unearned revenue should be entered into your journal as a credit to the unearned revenue account and as a debit to the cash account. This journal entry illustrates that your business has received cash for its service that is earned on credit and considered a prepayment for future goods or services rendered. As a result, the electric utility will have up to one month of expenses without the related revenue being reported. Therefore, at each balance sheet date, the utility must accrue for the revenues it earned but had not yet recorded. This is done through an accurual adjusting entry that debits a balance sheet receivable account and credits an income statement revenue account. When you receive unearned revenue, it means you have taken up front or pre-payments before the actual delivery of products or services, making it a liability.

- Once a company delivers its final product to the customer, only then does unearned revenue get reversed off the books and recognized as revenue on your profit and loss statement.

- At the end of April, the balance sheet will report the company’s remaining liability of $240.

- Learn the concept of unearned revenue, also known as deferred revenue.

- We only want to recognize revenue once specific tasks have been completed, which give us full claim to the money.

- There are a few additional factors to keep in mind for public companies.

However, with quarterly or annual contracts, customers often pay upfront, meaning that the company has received cash before providing the service—leading to unearned revenue on the company’s books. For most businesses where prepayment terms are 12 months or less, unearned revenue is treated as a current liability on the balance sheet. An example of unearned revenue is when someone signs a yearlong contract with a meal delivery service. The customer prepaid for a full year of meals, although they have not received all the meals. The customer can cancel their contract anytime before the meals are delivered, which makes unearned revenue or prepayments a liability to the company. Unearned revenue is most common among companies selling subscription-based products or other services that require prepayments. Classic examples include rent payments made in advance, prepaid insurance, legal retainers, airline tickets, prepayment for newspaper subscriptions, and annual prepayment for the use of software.

When is unearned revenue recognized?

Under cash accounting, the four thousand dollar sale would not be recognized as revenue until the twentieth, when the cash actually changed hands from the customer to the machine-selling business. Unearned revenue is recognized in accrual accounting, but not in cash accounting. When a company initially receives unearned revenue and has not yet provided the agreed good or service to the customer, this revenue is considered unearned revenue received. When the company provides the agreed good or service to the customer, and the terms of the agreement are considered fulfilled, the revenue is considered to be unearned revenue earned. The unearned revenue earned is then recognized as sales revenue on an income statement. For example, a contractor quotes a client $1000 to retile a shower. The client gives the contractor a $500 prepayment before any work is done.

- ASC 606 went into effect December 15, 2017, and it established a standard method by which companies record revenue in customer contracts.

- The complete, concise guide to winning business case results in the shortest possible time.

- Unearned incomeis income that a company receives from investments or other sources that aren’t related to its main business activities.

- After four months, the company can recognize 33% of unearned revenue in the books, equal to $400.

- Accounting is a process designed to capture the economic impact of everyday transactions.

Companies using the accrual method can make use of unearned revenue to help align income with costs and potentially defer income taxes until later periods when revenue has been earned. Only revenue that’s been earned or recognized shows up on the income statement. Over time, the liability gradually gets converted into income as the product or service gets delivered.

Unearned revenue is usually disclosed as a current liability on a company’s balance sheet. This changes if advance payments are made for services or goods due to be provided 12 months or more after the payment date.

Is unearned revenue accounts payable?

In the case of the Unearned Revenue, the account is supposed to be settled in exchange for goods and services, whereas in the case of Accounts Payable, the liability is settled with Cash.

For products received more than 12 months after purchase, companies must record this unearned revenue as a long-term liability. These types of companies need the unearned revenue of their customers to create a product or service that can be distributed back to them.

What types of industries and sectors have unearned revenue?

Unearned revenue is a liability to the entity until the revenue is earned. Recording unearned revenue is critical if you’re using the accrual accounting method and receiving a lot of advance payments. If a business didn’t account for unearned revenue in this way, and simply recognized all revenue when payment was received, then revenues and profits would both be overstated in that initial period. Then, in future periods, revenues and profits would be understated.

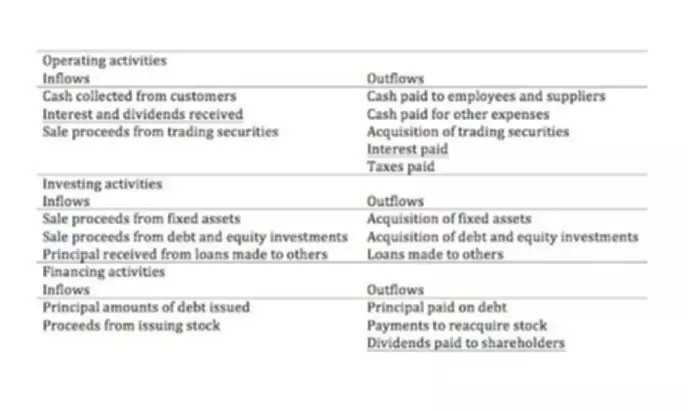

Financial StatementsFinancial statements are written reports prepared by a company’s management to present the company’s financial affairs over a given period . After deducting a portion of money from the unearned on your balance sheet, you can now add this to the total income revenue category on your balance sheet. The credit and debit are the same amount, as is standard in double-entry bookkeeping. There are several criteria established by the U.S.Securities and Exchange Commission that apublic companymust meet to recognize revenue. Since they overlap perfectly, you can debit the cash journal and credit the revenue journal. The statement of cash flows shows what money is flowing into or out of the company.